In the world of art making, most of us artists never learned about managing money. We often hear about the "starving artist," but it's time to get rid of that idea for good.

Managing your art money isn't some kind of magic trick. It's actually about learning some simple steps to get your finances in order. Here, we're going to show you the basics of how to start making your money work for you, not the other way around. It's all about getting organized and taking control, step by step.

The 6 Steps To Financial Literacy For Artists

STEP 1: SETTING FINANCIAL GOALS:

Setting financial goals is the first big step towards achieving financial stability and success. The most effective way to set these goals is by following the SMART criteria: Specific, Measurable, Achievable, Relevant, and Time-bound. READ OUR POST ABOUT GOAL SETTING

Start by clearly defining what you want to achieve, such as saving for a down payment on a house or building an emergency fund. Make your goals measurable by attaching numbers to them, for instance, "I want to save $10,000 in an emergency fund within two years."

Ensure your goals are achievable given your current resources and constraints, and relevant to your broader financial and personal aspirations. Finally, set a realistic timeline for each goal to keep yourself accountable and motivated. By breaking down your financial objectives into smaller, manageable steps and regularly reviewing and adjusting them as necessary, you can pave the way for a more secure and prosperous financial future.

Here is a simple roadmap for financial goal settings:

1) Set Goals

2) Understand where your money comes from and where your money goes

3) Set a budget

4) Get out of Debt and pay off high interest loans

5) Start saving your emergency fund

6) Start putting aside money for reitrement

7) Start saving for your dream (own your studio, dream trip, buying art)

STEP 2: Know Where Your Money Goes

Knowing where your money comes from and where it goes is the most important step to financial literacy. It involves dissecting your bank statements to distinguish between discretionary and fixed expenses.

This takes effort, but fortunately, it becomes simpler as time goes by. Consider the task of cleaning your house. If it's extremely messy, a deep clean might require a whole day's work. However, once you've laid the groundwork, a bit of maintenance every week or once a month can keep your home tidy.

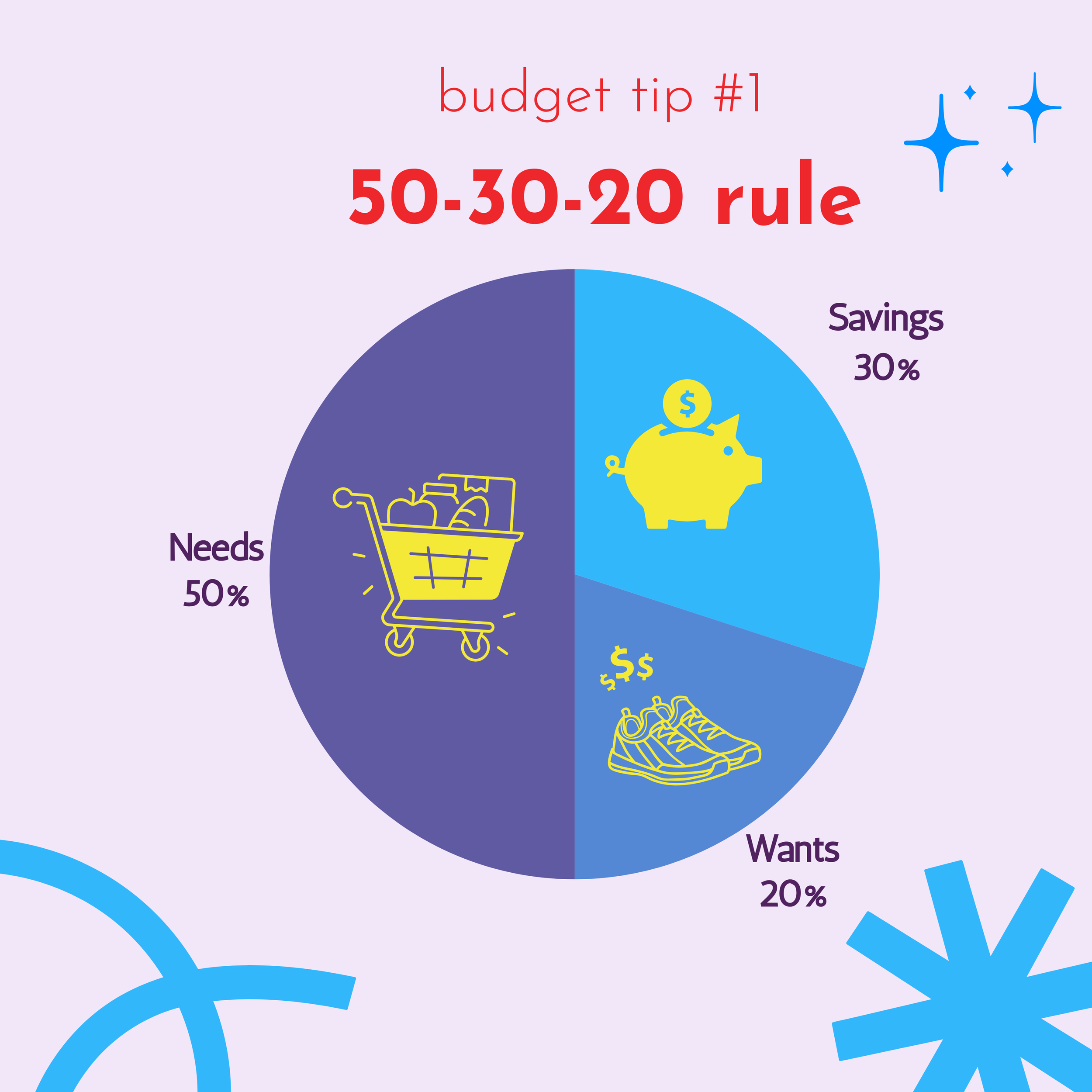

STEP 3: IS SETTING A BUDGET: the 50/30/20 rule

A typical budget balances your savings and living costs. This often follows a 50/30/20 rule (but will depend on your financial goals). The 50/30/20 rules is a straightforward framework designed to provide a healthy

50% of your net income should be allocated to necessities, which include housing, utilities, groceries, transportation, and other essential living costs. This portion ensures that all your fundamental needs are covered without stretching your finances too thin.

30% of your net income is designated for wants, which covers non-essential expenses such as dining out, entertainment, hobbies, and other discretionary spending. This segment allows for personal enjoyment and quality of life improvements while keeping spending in check.

20% of your net income goes towards savings and debt repayment. This includes contributions to emergency funds, retirement accounts, and paying off any high-interest or non-mortgage debt. This critical portion emphasizes the importance of building financial security and independence over time.

These percentages serve as a guideline and can be adjusted based on personal circumstances, goals, and financial responsibilities. The key is to ensure that you're living within your means and NOT BUILDING MORE DEBT. Prioritize savings, and manage your existing debt effectively, all while allowing room for personal enjoyment and fulfillment.

STEP 4: Building Your Emergency Fund

Building an emergency fund is a key step toward financial security. Many Americans struggle to cover a $400 emergency expense. Our aim is to create a safety net worth at least three months of your essential expenses. This buffer is crucial for artists, who may not have steady income streams. It provides a financial cushion during periods when art sales slow down or if you face unexpected job loss.

Starting small can still yield big rewards, even though saving three to six months' worth of expenses might seem overwhelming at first. It's also important to focus on paying off high-interest debt and starting to save for retirement as critical measures to safeguard your financial future.

Step 5: Embracing Retirement Planning ASAP

Here's a crucial tip to keep in mind: Starting your savings journey early is incredibly important. Even setting aside as little as $5 a week can significantly impact your retirement fund, potentially making the difference between having $500,000 or $1 million by the time you retire.

For retirement savings, options include Individual Retirement Accounts (IRA), Roth IRAs (highly recommended for artists), and employer-sponsored 401(k) plans. Don't fall for the myth that it's too late to start saving for retirement if you're an older artist. We urge artists of all ages to begin saving now.

Thanks to the power of compound interest, even small, regular savings contributions can accumulate into a large sum over the years.

INVESTING SOUNDS SCARY? USE A ROBO-ADVISOR!

And for those who find investing intimidating, the good news is that there are excellent robo-advisors available from platforms like Vanguard, Fidelity, and Betterment. These services handle all the investing complexities for a minimal fee, making it easy to set up a direct deposit and enjoy the peace of mind that comes from knowing your future is secure.

Step 6: Get a hold of your DEBT!

Understanding and effectively managing debt is your next big goal, particularly when it comes to high-interest debts like those from credit cards.

Start with a clear understanding of what you owe. List all your debts, including credit cards, student loans, auto loans, and any other obligations along with their interest. Once you have a comprehensive overview, the next step is setting specific, achievable goals for paying off these debts.

Financial experts often recommend the "avalanche" method, which involves focusing on paying down the debts with the highest interest rates first while maintaining minimum payments on others. This method can reduce the amount of interest you pay over time, making it a financially savvy strategy.

Remember, managing debt isn't just about paying it off; it's also about not accruing more. This means living within your means, avoiding unnecessary expenses, and ensuring that your spending habits don't undermine your debt repayment efforts. By adhering to these principles, you can work towards a future where debt doesn't control your financial destiny, paving the way for greater financial stability and independence.

Those are the basic steps to get your financial house in order! Once you tackle the basics its worth diving a little deeper into financial literacy.

Business Structures for artists: Sole Proprietor vs LLC

Many artists operate as sole proprietorships, essentially running a one-person business. As their financial success grows, a crucial next move is considering the formation of a Limited Liability Company (LLC). Establishing an LLC is beneficial for managing liability, particularly when expanding the business to include employees.

An LLC acts as a vital mechanism for delineating personal and business finances, thus protecting an artist's personal assets from any liabilities incurred by the business. This distinction becomes increasingly important for artists who take on staff, offering a layer of legal defense against potential workplace incidents or legal actions tied to the business operations.

TAXES

In general consulting with a tax professional is an essential step for artists. A tax advisor can offer tailored advice on the optimal timing for business structure changes based on an artist's income, growth trajectory, and tax situation. They can also provide guidance on maintaining compliance with state and federal regulations, which is crucial for avoiding penalties and maximizing tax benefits. Additionally, a tax professional can assist artists in navigating the complexities of self-employment taxes, potential write-offs, and strategies for financial growth. Ultimately, the guidance of a tax advisor, combined with a strategic approach to business structuring, empowers artists to focus on their creative work while ensuring their financial and legal affairs are in order.

The role of real estate as a goal

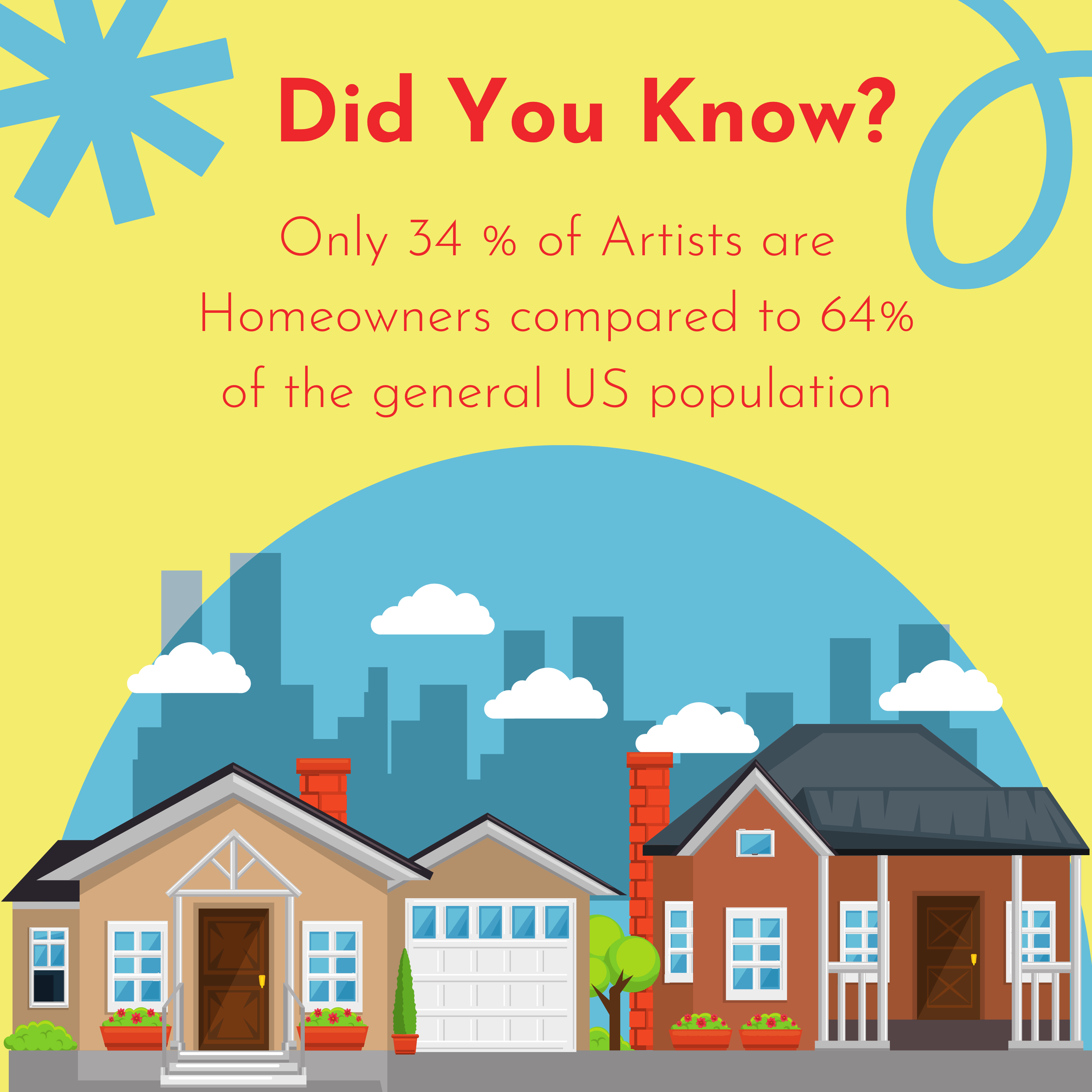

Real estate holds a unique position in the financial planning landscape for artists, often symbolizing a milestone of personal and financial achievement. Owning property can provide not only a stable living environment conducive to creativity but also act as a valuable asset in an artist's financial portfolio. However, the decision to invest in real estate necessitates careful consideration of one's career trajectory, income stability, and the ability to manage the ongoing costs associated with property ownership. According to a survey by the National Endowment for the Arts, only 34% of artists are homeowners, compared to 64% of the general U.S. population, underscoring the challenges many artists face in achieving this aspect of the American dream.

The integration of real estate into an artist's set of financial goals extends beyond the immediate benefits of ownership; it also involves understanding the impact on one's overall financial health and long-term goals. As Tamara Bates highlighted, artists must evaluate their readiness to commit to a property, factoring in market conditions, potential for property value appreciation, and the liquidity of real estate as an asset. For artists, who may experience fluctuating incomes, the flexibility and security offered by real estate must be balanced against the need for mobility and the freedom to pursue artistic opportunities. Thus, while real estate can play a pivotal role in building wealth and providing stability, it requires a strategic approach tailored to the unique circumstances of each artist's life and career.

Conclusion: Taking Control of Your Financial Future

By understanding where money flows, saving for emergencies, planning for retirement, managing debt wisely, and considering the implications of major purchases like real estate, artists can secure their financial future. This, in turn, frees them to focus on what they love most: creating art.

The journey to financial literacy for artists is not just about accumulating wealth; it's about ensuring that financial concerns do not impede creative expression.

For those interested in delving deeper into the intricacies of financial planning for artists, Tamara Bates's program, The Dots Between, offers a wealth of resources and guidance. Her insights provide a roadmap for artists navigating the often complex terrain of personal finance, ensuring they have the tools needed to thrive both creatively and financially.